What to Know About Lincoln Financial Claim Denials

Lincoln Financial disability claims are often denied due to biased in-house medical reviews, rigid interpretation of policy terms, and strict deadlines. Even loyal, long-term policyholders who have been paying regular premiums for years can fall victim to Lincoln disability insurance denials.

What's important to keep in mind: Lincoln Financial claim denials don't always reflect the validity of your case, and you do have the right to appeal their decision.

Find out more about Lincoln Financial disability denials:

- Today, the insurer provides coverage to about 17 million people across several products and is one of the largest long-term disability (LTD) insurance carriers in the country.

- Insurance companies have a legal duty to their policyholders to act in good faith and fair dealing. If Lincoln Financial has failed to uphold their end of the bargain, they may be acting in bad faith.

- Over the years, Lincoln Financial has been accused of wrongfully denying valid claims based on paper reviews that contradict a treating physician's opinion and targeting claims when the definition of disability changes from "own occupation" to "any occupation."

- Common reasons for Lincoln Financial claim denials include a lack of subjective medical evidence like MRIs for subjective illnesses, surveillance, and failure to meet policy deadlines.

- In one case, the insurer agreed to pay up to $117.7 Million to resolve claims that they improperly increased the cost of insurance for certain policyholders.

- Lincoln Financial complaints filed with the Better Business Bureau most frequently allege delayed claim processing, unresponsive case managers, and repeated documentation requests for records already submitted.

A Lincoln Financial denial can be frustrating and financially devastating, but a denial is not necessarily the end of the road. Our Lincoln Financial long-term disability lawyers can help families in all 50 states seek the benefits they deserve.

5 Reasons for Lincoln Financial Disability Denials

Lincoln Financial disability insurance claims can be denied for a variety of reasons, many of which have little to do with whether you’re unable to work. The insurer has been known to use certain tactics to avoid paying the benefits they owe.

Lincoln Financial long-term disability denials often result from a lack of objective medical evidence, insurer surveillance, or failure to meet the policy's definition of disability. Denials may be paid initially and then denied when the policy shifts from "own occupation" to "any occupation."

Lincoln Financial claim denial tactics may include:

- Insufficient Medical Evidence: Saying your medical records don’t show how your health condition prevents you from working and lack objective evidence like MRIs to back up your claim

- Change in Definition of Disability: Scrutinizing claims and terminating benefits when the policy's definition of disability changes from being unable to perform your "own occupation" to "any occupation," typically after the 24-month mark

- Surveillance or Social Media Monitoring: Using surveillance or reviews of your social media activity to look for evidence to contradict your reported limitations

- Paper-Only Reviews: Relying on doctors on their payroll to review your files and make medical assessments without ever examining you in person

- Missed Deadlines: Arguing that you failed to meet deadlines for submitting paperwork or filing an appeal, resulting in an automatic denial despite the merits of your claim

Lincoln Financial may use multiple tactics to make the process confusing and overwhelming, hoping that you'll give up and abandon your claim for the LTD benefits you've paid for.

However, the Lincoln Financial disability lawyers at Sokolove Law understand the tactics that the insurer may use to deny legitimate claims and how to counter them to secure the benefits policyholders deserve.

"At Sokolove Law, we’ve helped people nationwide challenge disability denials and recover the benefits they were rightfully owed. A bad faith insurance claim isn’t just about money — it’s about justice, accountability, and giving people the chance to move forward with dignity."

– Ricky LeBlanc, Managing Attorney of Sokolove Law

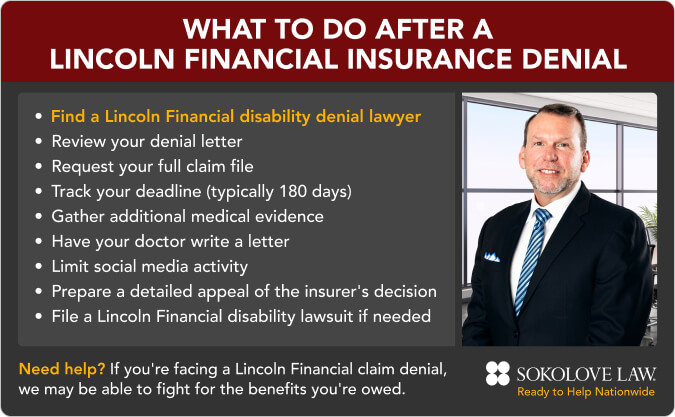

What to Do After a Lincoln Financial Group Long-Term Disability Denial

A denial isn’t necessarily a final answer. If your Lincoln Financial long-term disability claim has been denied, you have the right to file an appeal and even a lawsuit if needed.

Lincoln Financial disability denials are often the result of intentional obstruction or unfair demands regarding the paperwork you provide and when you provide it.

With 45+ years of experience successfully handling long-term disability cases, Sokolove Law is ready to step in and fight for the benefits you need and deserve.

If you're facing a Lincoln Financial LTD denial, we may be able to help you:

- Understand Your Rights Under ERISA: Most employer-sponsored disability plans are governed by the Employee Retirement Income Security Act (ERISA), which gives you the right to appeal a denial and requires insurers to follow certain rules.

- Make Sense of Your Denial Letter: The denial letter explains why Lincoln Financial rejected your claim and specifies the deadline to file an appeal.

- Obtain Your Claim File: You have the right to obtain your full claim file, which includes the evidence the insurer relied on in making their decision. Reviewing it can help identify gaps or weaknesses in your claim as well as provide strong evidence if we need to pursue a Lincoln Financial lawsuit.

- Strengthen Your Evidence: Updated medical records and doctor statements can show how your condition prevents you from working and confirm you're unable to perform job duties as expected.

- File a Timely Appeal: Your Lincoln Financial appeal should directly address the reasons for the denial, include any new supporting evidence, and be filed before any deadlines.

- Take Legal Action: In some cases, policyholders may be able to file a Lincoln Financial disability lawsuit to pursue the benefits owed.

With the long-term disability denial attorneys at Sokolove Law handling your case, you can focus on your recovery and moving forward with your life.

“Thanks to Sokolove Law, we won the battle against the insurance company. Now, I have the support and financial security I need to focus on my health and well-being. I’m grateful for their help and would recommend Sokolove Law to anyone facing a similar struggle.”

– Engineer in D.C. with a Denied Disability Claim

What to Expect with Your Lincoln Financial Disability Appeal

A Lincoln Financial disability appeal is an administrative process under ERISA, which requires the submission of new evidence within 180 days of your claim denial.

Lincoln will likely use internal or third-party medical reviewers to scrutinize your file and find minor discrepancies to uphold the insurer's decision.

The Lincoln Financial Group disability appeal process typically includes:

- Reviewing Your Denial Letter: Lincoln Financial’s denial letter will state why your claim was denied and when your appeal deadline expires.

- Requesting Your Claim File: Ask for a complete copy of your claim file to see what evidence was considered and what may have been overlooked.

- Strengthening Medical Evidence: Gather updated medical records, functional capacity evaluations, and detailed statements from your doctors to support your inability to work.

- Preparing Your Appeal: Submit paperwork for your appeal that directly addresses Lincoln Financial’s reasons for denial and clearly explains why you qualify for benefits.

- Undergoing Administrative Review: Lincoln Financial will review your appeal and may rely on internal or third-party medical reviewers on their payroll to reassess your claim.

- Receiving a Decision: Most appeal decisions are issued within 45 to 90 days, depending on the complexity of your case and other factors.

- Exploring Legal Options: If your appeal is denied, you may still have the right to file a lawsuit under ERISA to pursue the benefits you deserve. Claimants typically have 180 days from the date the denial was issued to file an appeal.

Challenging a Lincoln Financial disability denial can feel overwhelming, especially when you’re already dealing with a serious health condition. Our team can help families in all 50 states build strong appeals.

Call (800) 995-1212 now to see if our Lincoln Financial disability attorneys may be able to fight for your Lincoln Financial disability benefits. It costs nothing to speak with us.

Who Can File a Lincoln Financial Lawsuit?

A Lincoln Financial lawsuit may be possible if you’ve exhausted the company’s internal appeals process and were still denied the benefits you’re entitled to.

You may be able to file a Lincoln Financial lawsuit if:

- You were denied long-term disability benefits

- Attempts to appeal the company’s denial were unsuccessful

- The denial was unreasonable or not supported by the terms of your insurance policy

- There are medical records or other documentation supporting your disability

There’s only a limited amount of time to take legal action due to state laws called statutes of limitations, so it’s important to contact an attorney as soon as possible. Once the deadline in your case has passed, you may lose your right to seek justice.

How to File a Lincoln Financial Disability Insurance Appeal or Lawsuit

From filing paperwork to meeting deadlines, filing a Lincoln Financial LTD appeal or lawsuit after a denial involves set procedures that must be followed. When policyholders fail to meet these requirements, they're unlikely to be successful.

To appeal a denial from Lincoln Financial Group, you generally have 180 days to submit a written appeal under ERISA. Request your full claim file, then include new medical evidence, doctor support, and a clear rebuttal of the insurer’s reasons for denial.

At Sokolove Law, we help guide clients through every step of the process — from the initial appeal to a potential Lincoln Financial disability lawsuit.

1. Know Your Deadline

Most long-term disability policies give you a limited amount of time to file an appeal. Missing this deadline can put an immediate stop to your appeal and to securing any benefits that you may be owed.

Lincoln Financial Group policyholders typically have up to 180 days to file an appeal. However, the company has been known to delay issuing denial decisions or request repeated documentation, which can cut into the time you have to prepare your appeal.

Our team helps ensure all deadlines are met from the onset to the resolution of your case. This protects your right to seek benefits through an appeal or lawsuit.

2. Review Your Lincoln Financial Long-Term Disability Policy

A review of your Lincoln Financial long-term disability policy and denial letter will provide information on the reasons for your claim denial.

Our Lincoln Financial disability appeal lawyers can look at:

- The stated reasons for denial

- How the policy defines disability

- The information in your full claim file

- Any missing evidence

After reviewing this information, your lawyer can develop an appeal strategy to pursue the benefits you deserve.

3. Build and Submit a Thorough Appeal

Your Lincoln Financial disability appeal should be comprehensive, address each reason for denial, and be submitted before any deadlines.

Your appeal should include:

- A formal appeal letter that outlines why Lincoln Financial's decision is wrong

- Updated medical records to prove you cannot perform your job duties

- Letters from treating physicians that explain your restrictions and limitations

- Statements from family or co-workers detailing the impact of your disability

Our team can gather and present this information to build a strong case and make it more difficult for a Lincoln Financial appeal denial.

4. Wait for a Decision

After receiving the paperwork for your appeal, Lincoln Financial will issue a decision, typically within 45 to 90 days. We handle all communications with the insurance company, sparing you the back-and-forth.

When insurers delay processing or paying a claim, their actions may be considered bad faith, especially if the delay appears aimed at stalling benefit payments. In that situation, policyholders may be entitled to additional compensation beyond their benefits.

5. File a Lincoln Financial LTD Lawsuit If Necessary

If your appeal is denied, you may be able to file a second one or a Lincoln Financial disability lawsuit to seek the benefits owed.

Our Lincoln financial disability insurance lawyers can explain your options and file a lawsuit on your behalf if you meet the criteria.

Insurance companies like Lincoln Financial often have teams of attorneys tasked with defending their decisions. Having an experienced legal team on your side can help even the playing field.

Since 1979, Sokolove Law has helped thousands of families nationwide secure the compensation they deserve.

Get a Free Case Review

Lincoln Financial Disability Settlements & Verdicts

Lincoln Financial disability settlements and verdicts may vary based on the individual facts of each case. The strength of the medical evidence, your policy terms, and the nature of your disability can all play a role.

In some situations, you may be able to recover back benefits starting from the date your claim was denied, along with interest.

A few of our Lincoln Financial lawsuit settlements and verdicts include:

- $243,000 for a Maryland doctor denied Lincoln Financial disability

- $181,000 to a college worker whose doctors said he couldn't go back to work despite the insurance company's doctor insisting he could

- $175,000 for a California woman whose Lincoln Financial LTD benefits were unfairly terminated

- $128,000 to a Massachusetts woman whose LTD benefits were unfairly terminated after Lincoln Financial claimed she failed to meet the definition of a total disability despite her doctor's opinion

- $156,000 for a California man facing an unfair denial

- $160,000 to a university employee facing an unfair denial for lack of records after being injured during a traumatic delivery

While there's never a guarantee of compensation, our Lincoln Financial disability insurance lawyers will fight hard to get you everything you're entitled to.

These court results show that a claim denial is not always final and that a decision can be reversed when backed by strong supporting evidence.

Lincoln Financial Disability Lawsuit News & Updates

Lincoln Financial lawsuits and regulatory actions underscore how the insurance company handles claims. These cases show patterns in behavior and provide information for policyholders considering filing an appeal or taking legal action.

A few of the latest Lincoln Financial disability denial lawsuit updates include:

- The insurer agreed to pay up to $117.5 Million to life insurance policyholders after raising insurance costs.

- The U.S. Department of Labor required Lincoln Financial Group to reform their practices after finding it accepted premiums but later denied claims.

- Lincoln Financial paid a $12.6 Million settlement after being accused of failing to identify deceased policyholders and pay beneficiaries.

- The insurer paid $52 Million to policyholders in New York for lost insurance claims and unfair claims settlement practices.

$117 Million Lincoln Financial Settlement Over Life Insurance

More than 50,000 policyholders will share a $117.5 Million Lincoln Financial settlement resolving claims that the insurer improperly increased cost-of-insurance charges on certain life insurance policies.

The policyholders alleged the hikes were used to force policies to lapse and avoid paying benefits, though the insurer denied any wrongdoing.

The settlement ends over 6 years of litigation involving policies issued between 1983 and 2007. Eligible class members will receive cash payments based on excess charges they paid, with a minimum payout of $200.

Worker with COVID Secures Lincoln Financial Disability Settlement

In 2024, a lawsuit against Lincoln Life Assurance, a subsidiary of Lincoln Financial, was resolved after a worker alleged his long-term disability benefits were wrongly terminated while he battled long COVID.

The Lincoln Financial disability lawsuit was filed under ERISA in Massachusetts federal court. The policyholder, who reportedly suffered from shortness of breath and fatigue, initially received LTD benefits until the insurer cut them off.

Lincoln Financial reinstated benefits after the lawsuit was filed and after they had considered additional documentation, according to Law360.

Lincoln Financial Lawsuit Results in Reinstatement of LTD Benefits

A lawsuit against Lincoln National Life Insurance Company challenged the denial of long-term disability benefits to a senior payroll specialist at Alive Hospice in Nashville, Tennessee with fibromyalgia and other chronic conditions.

The insurer determined she was not “totally disabled,” relying on internal medical reviewers who said she could still perform sedentary work, according to the court filing.

However, the judge ruled in favor of the policyholder on the basis that fibromyalgia cannot be confirmed through objective testing and that the insurer improperly discounted the opinions of the woman's treating physicians.

"Thus, the Court concludes that Lincoln National's rejection of the treating physicians' opinions on Plaintiff's ability to work was arbitrary and capricious."

– U.S. District Judge William J. Haynes, Middle District of Tennessee

Lincoln Financial Settlement Results in Claim Practice Changes

In 2024, the U.S. Department of Labor reached a settlement with Lincoln Financial Group requiring major changes to how the company handles evidence of insurability (proof of good health) for employer-sponsored life insurance plans.

Under the Lincoln Financial settlement:

- Lincoln cannot deny claims for lack of insurability if premiums were paid for 3 months or more.

- The company must request proof of insurability within the first year of coverage.

- Lincoln cannot use health conditions that arise after premiums begin to deny eligibility.

- The insurer agreed to reprocess denied claims dating back to 2018.

The investigation found Lincoln had accepted premium payments for months or even years, then later denied death benefits because policyholders had not provided proof of insurability.

3rd Circuit Finds Lincoln Financial Wrongfully Denied Disability Benefits

In 2024, a federal appeals court ruled that Lincoln Financial Group improperly terminated a coal miner's long-term disability benefits.

The 3rd Circuit determined that the insurer failed to adequately prove that the Consol Energy Inc. employee could perform alternative work under the policy’s “any occupation” standard after an ankle injury.

The ruling highlighted issues with how Lincoln evaluated the claimant’s qualifications, including relying on inaccurate job assumptions and overstating transferable skills. As a result, the court ordered the reinstatement of benefits.

$12.6 Million Lincoln Financial Settlement Over Death Master File Practices

Lincoln National Life Insurance Company and their affiliates agreed to pay $12.6 Million to settle claims from multiple states that they failed to identify deceased policyholders and pay life insurance benefits to beneficiaries.

Regulators alleged the company used the Social Security Administration’s Death Master File (DMF) to stop annuity payments — but did not use it to locate unpaid life insurance claims, pocketing the money instead.

Under the settlement, Lincoln Financial must regularly compare their policy records against the DMF to ensure beneficiaries are identified and paid in a timely manner. The company is also required to submit ongoing reports and undergo follow-up regulatory review.

$52 Million Lincoln Financial Settlement Over Delayed Insurance Claims

Lincoln Financial Group agreed to pay $52 Million to resolve allegations by the New York State Department of Financial Services that they mishandled life insurance policies following their merger with Jefferson-Pilot.

Regulators claimed system integration failures caused the company to lose track of thousands of policies, leading to significant delays in paying claims. As part of the settlement, Lincoln paid $50.7 Million total to customers and a $1.5 Million fine.

Some policyholders reportedly waited months or even years for benefits due to backlogs and processing issues tied to outdated systems and inadequate employee training.

Lincoln Financial Long-Term Disability Complaints

Lincoln Financial policyholders across the country have reported troubling patterns in the way their claims are handled and the delays or denials that usually follow.

Documented through Better Business Bureau filings, consumer reviews, and court records, Lincoln Financial complaints paint a consistent picture of a company that makes an already difficult process even harder.

Here are 5 common Lincoln Financial LTD complaints:

- The definition of "disabled" doesn't always mean what policyholders were told: Multiple policyholders have reported that Lincoln Financial interpreted their policy's disability definition in ways that felt inconsistent with what they were told when they enrolled.

- Delays that create serious financial hardship: Some policyholders report waiting weeks or months for Lincoln Financial to respond to claims or appeals, even after submitting complete documentation.

- Denials that make a hard time even harder: Policyholders consistently describe a flawed claims process, such as case managers who don't return calls, denials without clear explanations, and new justifications that only appear after a lawsuit is filed.

- Requests for excessive or repetitive documentation: Lincoln Financial allegedly asks for more paperwork than required — then asks for it again. Courts and consumer complaints indicate a pattern of documentation requests being used as a tool to avoid paying benefits.

- Denials based on reviews that never involved a real examination: Lincoln Financial routinely relies on in-house physicians and third-party reviewers who never examine the claimant in person. These paper reviews can unfairly dismiss treating physicians' opinions.

Better Business Bureau complaints cite poor communication, unresponsive case managers, and a review process that feels designed to exhaust rather than evaluate. Lincoln Financial complaints most often reference unreturned phone calls, stalled claims, and unclear denials.

One policyholder alleged that despite submitting 6 medical notes from 3 providers, CT scans, lab results, medical restrictions, and written confirmation from their employer that they could not return to work, they were told repeatedly that more documentation was needed.

How Our Lincoln Financial Disability Insurance Lawyers Can Help

When Lincoln Financial denies your long-term disability claim, it can feel like the system is stacked against you. Tight deadlines, confusing policy language, and unhelpful claims agents can make it difficult to know what to do next.

That’s where working with a Lincoln Financial disability benefit attorney from Sokolove Law can make a real difference. Having an experienced legal team on your side may help improve your chances of securing the benefits you deserve.

A Lincoln Financial denial attorney on our team can:

- Break Down Your Lincoln Financial Denial Letter: These letters often rely on technical language and cherry-picked evidence. We help you understand exactly why your claim was denied — and what’s needed to challenge it.

- Build a Strong, Evidence-Backed Appeal: Successful appeals require more than basic medical records. We gather detailed physician reports, specialist opinions, and vocational evidence to clearly show how your condition limits your ability to work.

- Manage the Entire Appeals Process: Before filing a lawsuit, most disability policies require you to complete a formal appeal. Our Lincoln Financial disability attorneys handle every step, including submitting documentation, meeting deadlines, and communicating directly with the company.

- Take Legal Action If Necessary: If your Lincoln Financial appeal is denied, we can file a lawsuit against the insurer and continue fighting for your benefits in court.

Insurance companies like Lincoln Financial have resources and legal teams to defend their decisions. You shouldn’t have to face that process alone.

At Sokolove Law, we work to level the playing field against powerful corporations. With no upfront costs or hourly fees, you can focus on your health while we handle the legal fight.

Find a Lincoln Financial Disability Lawyer Near You

As a national law firm, we have the resources and experience to help individuals facing an unfair Lincoln Financial denial, regardless of where they’re located in the United States.

Our Lincoln Financial disability lawyers can help families in all 50 states:

- Alabama

- Alaska

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming

Insurance companies have entire teams working around the clock to protect their profits. You deserve someone fighting just as hard for you and the benefits you’ve paid for. Contact us now to find a Lincoln Financial lawyer near you.

Get Help with Your Lincoln Financial Long-Term Disability Appeal

With Sokolove Law, you'll have peace of mind knowing that your Lincoln Financial appeal is in good hands. If you have a case, we can handle every step of the appeals process on your behalf, so you can go about your daily routine.

Why choose the Lincoln Financial disability attorneys at Sokolove Law?

- Over 45 years of experience

- More than $148 Million total secured for clients nationwide

- No upfront costs or out-of-pocket fees

Call (800) 995-1212 now or fill out our contact form for a free, no-obligation legal consultation.

Lincoln Financial Disability Benefit Denial FAQs

Can I appeal a Lincoln Financial long-term disability denial?

Yes. If you're facing a wrongful Lincoln Financial long-term disability denial, you may be able to file an appeal directly with the insurance company.

Many families work with a disability lawyer to help ensure they meet deadlines and that their appeal is properly prepared and contains strong supporting evidence.

However, there are strict deadlines for filing a Lincoln Financial appeal, so it's crucial to seek legal help as soon as possible. Get started now with a free case review.

How does Lincoln Financial long-term disability work?

Lincoln Financial's long-term disability insurance is meant to replace part of your wages if you become unable to work due to a covered injury or illness.

Here’s how Lincoln Financial disability insurance typically works:

- You experience a health condition that falls under your policy’s definition of “disability”

- You file a claim and include supporting evidence like medical and job records

- After a waiting period, you may be entitled to Lincoln Financial short-term disability

- If approved, benefits begin and typically replace about 60% of your income

- Payments continue for a certain amount of time, usually a few years or up to retirement age, based on the terms of your policy

- While some plans pay benefits if you can’t perform your job, others require that you be unable to work in any job.

In some cases, policyholders receive benefits for a set period but then face termination suddenly. Over time, Lincoln Financial may scrutinize your claim to look for reasons to cut off benefits and boost their bottom line.

Does Lincoln Financial deny long-term disability claims?

Like many disability insurance companies, Lincoln Financial has been accused of unfairly denying valid long-term disability claims by using tactics like relying on in-house medical reviews, cutting off benefits at the 24-month “any occupation” changeover, and citing a lack of objective medical evidence for conditions like chronic pain.

If Lincoln Financial denied your claim, our long-term disability lawyers may be able to file an appeal on your behalf. Call (800) 995-1212 now.

How long does Lincoln Financial long-term disability last?

Long-term disability benefits from Lincoln Financial Group can last anywhere from a few years to retirement age. It all depends on the terms of your specific policy.

However, benefits can end earlier if Lincoln Financial determines you no longer meet their definition of disability, if medical evidence is deemed insufficient, or if certain policy limitations apply. In these cases, an attorney may be able to help you appeal and access your benefits again.

How long does it take Lincoln Financial to approve a claim?

Lincoln Financial may review a new claim within 3-5 business days, but a final decision on disability benefits often takes up to 45 days or longer.

Here's what to expect with a Lincoln Financial Group approval timeline:

- Initial review: A claims examiner may look at your submission within 3-5 business days.

- Early decision window: Some claims are approved, denied, or put on hold within the first few days of review

- Full decision timeline: Insurers typically have between 45 and 90 days to make a determination

- Documentation delays: If medical records or doctor responses are slow, the process can take longer or even lead to a denial

Delays are common, especially when Lincoln Financial requests additional documentation or reviews files multiple times to look for any reason to deny a claim.

Why did Lincoln Financial deny my long-term disability claim?

A denial from Lincoln Financial Group can feel confusing, but most denials come down to a handful of common issues tied to restrictive policy language and very specific demands for evidence.

Here are some of the most frequent reasons:

- Insufficient medical evidence: Your records may not clearly show how your condition limits your ability to work, even if you’re receiving treatment.

- Not meeting the policy’s definition of disability: Many plans shift from an “own occupation” standard to an “any occupation” standard after a year or more, making it harder to qualify.

- Pre-existing condition exclusions: If your condition was treated or diagnosed before coverage began, your policy may limit or deny benefits.

- Missed deadlines or incomplete paperwork: ERISA-governed plans have strict timelines, and even small errors can lead to a denial.

- Surveillance or social media reviews: Insurers sometimes use photos, videos, or online activity to argue you’re more capable than your claim suggests.

- Paper-only reviews: Instead of examining you in person, the insurer may rely on internal doctors who review records and disagree with your treating physician.

- Not a covered disability: The insurer may argue your diagnosis doesn’t meet the policy’s definition of a qualifying condition.

- Treatment not medically necessary: Procedures or care may be labeled elective, leading to denied benefits.

A denial doesn’t always mean your claim isn’t valid. Because Lincoln Financial has teams focused on limiting payouts, pushing back with a well-supported appeal can make a meaningful difference in the outcome.

What are Lincoln Financial long-term disability qualifications?

It depends on your policy, but in most cases, you must have a health condition that prevents you from working.

Conditions that may be covered by Lincoln Financial include:

- Cancer

- Carpal tunnel syndrome

- Cerebral palsy

- Chronic fatigue syndrome (CFS)

- Crohn’s disease

- Degenerative disc disease

- Diabetes

- Epilepsy

- Fibromyalgia

- Heart disease

- Lupus

- Mental health conditions, including anxiety and depression

- Multiple sclerosis (MS)

- Musculoskeletal disorders, like back or joint injuries

- Neurological conditions, including stroke or Parkinson’s disease

Unfortunately, even if you’ve been diagnosed with one of these conditions, Lincoln Financial may still claim that you're not entitled to benefits.

In these cases, a Lincoln Financial disability attorney may be able to file an appeal or lawsuit to pursue the benefits you’re owed.

How do I fight a Lincoln Financial claim denial?

Fighting a Lincoln Financial claim denial often involves consulting with a long-term disability denial lawyer, submitting a strong appeal backed by legal evidence, and filing a lawsuit against the insurer if needed.

An experienced Lincoln Financial disability attorney can handle all the legal work involved in an appeal while you focus on your recovery. Call (800) 995-1212 to see if we can fight for you.

Can I file a Lincoln Financial disability insurance lawsuit over a denied claim?

Potentially, yes. If Lincoln Financial denied your claim and you’ve exhausted the appeals process, you may qualify to file a Lincoln Financial disability lawsuit. In 2024, a Virginia coal miner won a reinstatement of LTD benefits after an ankle injury prevented him from working.

Only an experienced lawyer can determine if you may have grounds for a lawsuit. Call (800) 995-1212 now to see if you may qualify.

How much do Lincoln Financial disability attorneys cost?

At Sokolove Law, there are no upfront costs or hourly fees to work with our Lincoln Financial disability appeal lawyers. We work on a contingency-fee basis, meaning we only get paid if your case results in compensation.

How long does Lincoln Financial pay long-term disability?

It depends on your specific policy, but most Lincoln Financial Group long-term disability plans pay benefits for a set period or until you reach retirement age — as long as you continue to meet the policy’s definition of disability.

However, Lincoln has been known to reassess eligibility every few months and stop benefits if they determine a policyholder is no longer disabled.

Why is Lincoln Financial being sued?

Lincoln Financial Group has faced lawsuits for a range of issues, but most claims fall into a few key categories: denied benefits, policyholder overcharges, and mishandling of customer or investor funds.

Lincoln Financial lawsuits have involved:

- Wrongful claim denials: The company has been accused of ignoring medical evidence or improperly terminating disability benefits without sufficient support.

- Charging policyholders too much: Lincoln has paid over $100 million in settlements tied to allegations it improperly increased charges on life insurance policies.

- Improper claim practices: A U.S. Department of Labor investigation found Lincoln collected premiums for months or years, then denied benefits due to missing paperwork.

- Other legal actions: The company has also faced lawsuits involving retirement plan mismanagement, data breaches, and investor disclosures.

Most Lincoln Financial disability lawsuits center on whether the insurer treated policyholders fairly and followed their own policies when paying claims.

When does Lincoln Financial pay for short-term disability?

Lincoln Financial Group short-term disability benefits typically begin after you satisfy an elimination period.

Here’s how it usually works:

- Most Lincoln Financial STD plans require you to be out of work for 7 to 14 days before benefits start.

- Once your claim is approved and the elimination period is met, benefits are often paid weekly or biweekly, but the first check may take a few weeks while the claim is processed.

- You must provide medical evidence showing you’re unable to perform your job due to illness or injury.

If your Lincoln Financial short-term disability is denied, a lawyer may be able to fight for the benefits owed.