What to Know About Prudential Disability Denials

Prudential has built their brand around "the rock," a symbol of strength and stability. However, for policyholders whose disability claims have been delayed, underpaid, or denied, that image can feel inaccurate.

Behind the marketing, Prudential is a publicly traded corporation with a financial incentive to minimize payouts, and claimants with long-term disability (LTD) claims are often the ones who bear the cost.

If Prudential has cut off or denied your disability benefits, you still have options. You may be able to appeal the decision or pursue a lawsuit to recover the benefits you paid for.

Here's what every Prudential policyholder should know:

- Prudential routinely denies valid disability claims, according to court filings. The Fortune 500 company reported net income of $3.576 Billion in 2025, and minimizing payouts to policyholders is one way that number stays high.

- Prudential policyholders report encountering unexplained delays, medical reviews by doctors who never examined them, covert surveillance, and abrupt benefit terminations after months or even years of receiving payments.

- About 68% of disability applications are denied on the first attempt, meaning that claimants who fail to push forward may miss out on the benefits they're owed.

- Group disability coverage is issued through Prudential's subsidiary, The Prudential Insurance Company of America. This Newark, NJ-based entity is a defendant in disability lawsuits filed in federal courts across the country.

- A federal appeals court called Prudential's policy deadline language "labyrinthine" and "designed to confuse" — language structured so a claimant's window to sue can expire before they realize the clock has even started.

- Many employer-sponsored Prudential LTD policies are governed by ERISA, which imposes strict appeal deadlines. Missing those deadlines can eliminate your right to benefits.

- Prudential disability denials can be appealed or challenged in federal court through a lawsuit.

Prudential has teams of claims adjusters, company-hired physicians, vocational consultants, and defense attorneys focused on protecting the company's decisions and their bottom line.

"At Sokolove Law, we regularly assist people after a long-term disability denial by analyzing the insurer’s reasoning, identifying the weaknesses in their decision, and building the strongest appeal possible on our clients’ behalf."

– Ricky LeBlanc, Managing Attorney of Sokolove Law

At Sokolove Law, our Prudential disability lawyers can counter those tactics by assembling medical records, navigating procedural rules, hitting critical appeal deadlines, and taking Prudential to court when they refuse to pay what you're owed.

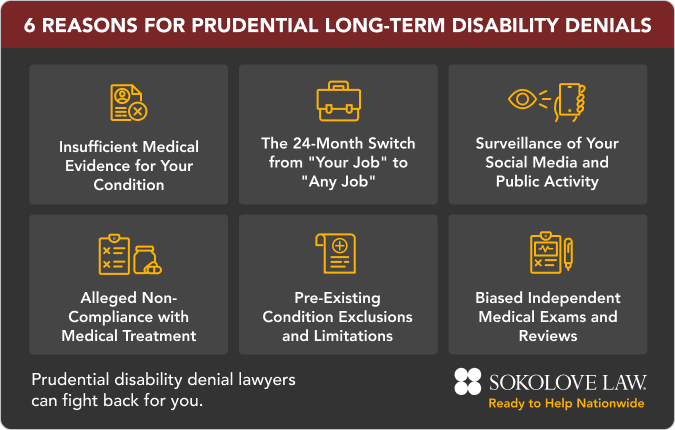

6 Reasons for Prudential Long-Term Disability Denials

Prudential long-term denials frequently come down to disputed medical evidence, policy language that shifts over time, and biased surveillance reports.

The company may argue that your records don't adequately document how your condition limits your ability to work, that you're capable of performing some type of job even if not your own, or that a technical deadline was missed.

Prudential benefit denial tactics may include:

- Insufficient Medical Evidence: Even with a formal diagnosis of a qualifying health condition, Prudential may demand test results that show exactly how your disability limits your ability to work. A doctor's note or a list of symptoms is rarely enough on its own.

- The 24-Month Definition Switch: Most LTD policies open with an "own occupation" standard, then flip to a far stricter "any occupation" test at the 2-year mark, a transition that has been used to cut off claimants who remain genuinely unable to return to any meaningful work.

- Surveillance and Social Media Monitoring: Prudential investigators may follow you, film you, or search your public profiles for anything that can be used to argue your actual abilities contradict what your medical records show, including a single photo taken on your best day.

- Treatment Non-Compliance: Gaps in treatment can be framed as a failure to pursue recovery, giving grounds for denials that have nothing to do with the severity of your actual limitations.

- Pre-Existing Condition Exclusions: If your disabling condition was diagnosed or treated in the months before your coverage took effect, it may be excluded from coverage entirely, regardless of how much it has progressed.

- Biased Independent Medical Exams: Rather than deferring to the physicians who have actually examined and treated you, Prudential routinely relies on contracted reviewers who assess your file without ever seeing you in person.

These tactics are rarely used in isolation. The combination of delayed decisions, shifting standards, and procedural complexity is often designed to make the process feel impossible and to make giving up feel easier than fighting back.

Our team knows how Prudential denials are built, and we know how to take them apart to get the best results possible for our clients.

What Can I Do After a Prudential Disability Benefit Denial?

A Prudential long-term disability denial may feel overwhelming, but it doesn't necessarily end your claim. Under ERISA, disability policyholders have the right to challenge the decision through an internal appeal and pursue their case in federal court if needed.

After a Prudential disability denial, you'll likely want to work with an experienced legal team that can build your case and file a detailed appeal within 180 days of receiving your denial letter.

Our Prudential disability insurance attorneys may be able to:

- Analyze Your Prudential Denial Letter: Prudential must explain why your claim was denied. Carefully reviewing the denial letter can help identify issues like missing evidence, surveillance findings, conflicting medical opinions, or disputes over your ability to work.

- Gather Stronger Supporting Evidence: Successful Prudential appeals often depend on building a more complete record. This may include updated medical records, specialist evaluations, diagnostic testing, medication histories, and physician statements explaining how your condition limits your ability to work.

- Address “Any Occupation” Findings: Prudential may argue that you can still perform another type of work, even if you can't return to your previous job. Additional vocational evidence or functional capacity evaluations may help challenge these conclusions.

- Prepare and File Your ERISA Appeal: Under ERISA, you typically must complete the internal appeals process before filing a Prudential disability lawsuit. A thorough appeal can address weaknesses in the original claim and include the evidence needed to support future legal action if necessary.

- Protect Critical Filing Deadlines: Missing the appeal deadline could jeopardize your ability to recover benefits. Most ERISA disability policies require appeals to be filed within 180 days of receiving the denial notice.

- Build the Strongest Case Possible: A Prudential long-term disability denial lawyer can help organize medical evidence, respond to insurer arguments, and develop a strategy tailored to the specific reasons your claim was denied.

Our experienced Prudential long-term disability denial attorneys can help you navigate every step of an appeal or lawsuit, build a stronger record, and ensure important evidence and deadlines are not overlooked.

"Thanks to Sokolove Law, we won the battle against the insurance company. Now, I have the support and financial security I need to focus on my health and well-being. I'm grateful for their help and would recommend Sokolove Law to anyone facing a similar struggle."

– Engineer with a Denied Disability Claim

What to Expect with a Prudential Disability Appeal

Under ERISA, Prudential disability claimants must complete the company’s internal appeal process before filing a lawsuit in federal court.

The appeal is also typically your final opportunity to submit new evidence into the record. Once Prudential closes the appeal file, courts often will not consider additional medical documentation later on.

Here's what a Prudential long-term disability appeal often involves:

- Requesting Your Claim File: One of the first steps is requesting your complete Prudential claim file. Under ERISA, Prudential must provide the records they relied on to deny your claim, including internal medical reviews, vocational assessments, surveillance materials, and claim notes.

- Working Within the 180-Day Deadline: In most cases, you have 180 days from the date of your denial letter to file your appeal. Missing this deadline could permanently prevent you from challenging Prudential’s decision or recovering benefits.

- Gathering New Supporting Evidence: The Prudential disability appeal process is often your best and sometimes last chance to strengthen your claim with updated medical records, diagnostic testing, specialist evaluations, and detailed physician statements.

- Challenging Prudential’s Vocational Findings: Prudential may argue that you can still work in another occupation, even if you cannot return to your previous job. Independent vocational experts can help evaluate whether those conclusions accurately reflect your physical, cognitive, or functional limitations.

- Waiting Through the Review Process: After your appeal is submitted, Prudential generally has 45 days to make a decision. However, ERISA regulations may allow the company to extend the review period for an additional 45 days, meaning many appeals take up to 90 days for a final determination.

The Prudential appeal process is meant to be confusing and difficult, with the goal of getting policyholders to just give up the benefits they paid for. Our team can help manage the entire process and fight for the benefits you deserve.

Call (800) 995-1212 now to see if we may be able to help with your Prudential disability denial. It costs nothing to speak with us.

Who Can File a Prudential Denial Lawsuit?

Policyholders whose LTD benefits were denied or terminated may have the right to file a Prudential disability lawsuit. However, before taking legal action, most claimants must first complete Prudential’s internal appeals process.

You may be eligible to file a Prudential denial lawsuit if:

- Prudential unfairly denied your long-term disability claim

- Your disability benefits were wrongfully terminated after previously being approved

- Prudential upheld the denial after your ERISA appeal

Prudential disability lawsuits are subject to strict deadlines known as statutes of limitations. Missing these deadlines could prevent you from pursuing benefits in court and accessing the compensation you deserve.

How to Fight a Prudential Long-Term Disability Denial

Filing a Prudential disability appeal or lawsuit involves unforgiving deadlines, detailed evidence, and complex ERISA rules. The way your appeal is handled can directly affect whether you're able to recover the disability benefits owed.

At Sokolove Law, we help clients navigate every stage of the process — from challenging a Prudential denial through the appeal process to pursuing a legal claim in federal court.

1. Review Your Prudential Denial Letter

Your denial letter explains why Prudential denied your claim and outlines the deadline for filing an appeal. In most ERISA disability cases, you have only 180 days from the date of the denial letter to submit your appeal.

Because ERISA appeals are mandatory before filing most Prudential LTD lawsuits, understanding the insurer’s reasoning from the start is critical.

Our team can review your denial letter, identify weaknesses in Prudential’s claim decision, and determine what evidence may be needed to strengthen your claim.

2. Request Your Claim File

A careful review of your Prudential disability policy and claim file can help uncover why your claim was denied and what evidence may be needed to strengthen your appeal.

Our Prudential disability denial lawyers can review:

- Prudential’s stated reasons for denying benefits

- The policy’s definition of disability

- Medical and vocational reviews relied on by Prudential

- Internal claim notes and communications

- Potential gaps, inconsistencies, or overlooked medical evidence

Understanding how Prudential evaluated your claim is often one of the most important parts of building an effective appeal strategy.

3. Submit a Prudential Disability Appeal

The administrative appeal is usually your last opportunity to add evidence to the claim record before litigation. In many Prudential lawsuits, courts later reviewing the case may only consider the evidence already included in the administrative file.

A strong Prudential long-term disability appeal may include:

- A detailed letter directly responding to Prudential’s denial reasons

- Updated medical records and specialist evaluations

- Detailed physician statements describing work-related limitations

- Reports from vocational experts that challenge Prudential’s assessment of your ability to work

Prudential generally has 45 days to review the appeal but may extend the process for an additional 45 days under ERISA, meaning many appeals take up to 90 days for a final decision.

4. File a Prudential Disability Insurance Lawsuit

If Prudential denies your appeal, you may be able to file a lawsuit in federal court. Unlike many other types of lawsuits, these cases are typically decided by a judge rather than a jury.

Because courts frequently limit review to the evidence already submitted during the appeal, building the strongest possible record before a Prudential lawsuit is extremely important.

Prudential has experienced legal teams dedicated to defending disability claim denials, which can make the process challenging. Our Prudential claim denial attorneys can explain your options and pursue the disability benefits you deserve.

Since 1979, Sokolove Law has helped thousands of families nationwide secure the compensation they deserve.

Get a Free Case Review

Prudential Disability Settlements & Verdicts

Prudential disability settlements and verdicts differ based on the details of each claim. Factors like the medical condition, quality of supporting evidence, terms of the policy, and the length of time benefits were withheld may affect case values.

In some situations, successful claimants may be able to recover past-due disability benefits, ongoing monthly payments, and interest on benefits that were wrongfully denied or terminated.

Our Prudential disability settlements and verdicts include:

- $579,000 for a Florida pharmacist whose Prudential benefits were terminated after 2 years

- $300,000 to a Virginia railroad worker who was told he could still do sedentary work

- $128,000 for a California man denied benefits after a year

- $200,000 to a California woman denied benefits after the company no longer considered her disabled

- $160,000 for a Georgia nurse who was denied after 2 years when the company insisted she could do sedentary work

- $230,000 to a Tennessee man with chronic pain who was denied after a year and a half

These results show that policyholders may still have a path to benefits following a wrongful Prudential LTD denial. While there's never a guarantee, our Prudential disability appeal lawyers will fight hard for everything you're entitled to.

Prudential Disability Insurance Lawsuit News & Updates

Prudential's record with disability and insurance claims has drawn attention from federal regulators and courts across the country. Courts have criticized Prudential's claims handling and even ordered the insurer to change their practices after a federal investigation.

Prudential disability insurance lawsuit updates include:

- A Colorado federal court ordered Prudential to reinstate disability benefits and pay all past-due amounts with interest after the company overrode the opinions of 16 health care professionals (Paquin v. The Prudential Insurance Company of America, D. Colo. 2018).

- The U.S. Department of Labor reached a settlement with Prudential after investigators found the company collected insurance premiums from policyholders for years then denied hundreds of claims when coverage was needed most.

- The U.S. Court of Appeals for the 1st Circuit called Prudential's lawsuit deadline scheme "labyrinthine" and "designed to confuse" after the company structured their limitations clock to expire before a claimant could reasonably sue (Smith v. Prudential Insurance Company of America, 1st Cir. 2023).

- A Kansas federal court rejected Prudential's interpretation of their own disability policy as bordering on "frivolous," finding it would automatically deny benefits to any claimant whose employment ended as a result of their disabling condition (Kennedy v. Foley Industries, D. Kan. 2024).

- A California court overturned a Prudential LTD denial for a woman with fibromyalgia, finding she had met her burden of demonstrating total disability under her plan (Przybyla v. Prudential Insurance Company of America, N.D. Cal. 2025).

Recent lawsuits and regulatory actions continue to put Prudential's policies and practices under increased scrutiny.

From manipulative deadline structures to the dismissal of treating physicians' opinions, Prudential disability denials follow patterns that experienced attorneys recognize — and know how to counter.

Court Orders Prudential to Reinstate Benefits after 16 Doctors Support Disability Claim

After contracting encephalitis from a West Nile virus-infected mosquito, a Colorado man sustained brain damage that ended his career as a business development director, according to the lawsuit.

Prudential paid his disability benefits for 11 years before ordering an independent exam and using it to terminate his claim. Two appeals failed, and he filed a disability lawsuit against Prudential.

Sixteen health care professionals, including one physician hired by Prudential, supported a finding of disability. Prudential's denial rested on 3 company-hired doctors. The court ordered payment of all past-due benefits with interest and the reinstatement of benefits going forward.

DOL Finds Prudential Collected Premiums for Years, Then Denied Claims

The U.S. Department of Labor's Employee Benefits Security Administration found that from 2017 to 2020, Prudential denied more than 200 life insurance claims on the grounds that participants failed to provide evidence of insurability.

However, Prudential had been collecting premiums from those same participants through payroll deductions, in some cases going back to at least 2004, without ever obtaining that documentation, according to investigators.

DOL Solicitor of Labor Seema Nanda called the practice "egregious," stating it "left grieving families without the life insurance for which their loved ones had paid, in some cases, for many years." Prudential was required to revise their practices and pay previously denied claims.

Court Calls Prudential Policy 'Designed to Confuse'

A Rhode Island accountant and vice president of tax operations for a technology company was reportedly diagnosed with a cognitive impairment, and a physician determined he could no longer work as a tax professional.

He left his job and filed a disability claim with Prudential. The insurer approved the claim and began paying a monthly benefit of $3,000 for nearly 2.5 years, according to the lawsuit.

However, Prudential notified the man that his benefits were being terminated effective the following day. Prudential's policy set a 3-year deadline to file a lawsuit, but started that clock on the date he was required to submit proof of disability, not on the date Prudential stopped paying his benefits.

Writing for the 1st Circuit, Judge Julie Rikelman noted that the court had previously characterized identical limitations schemes as "labyrinthine" and "designed to confuse." Prudential later settled the case.

Court Rejects Prudential's Disability Denial

After suffering a disability, an employee filed a claim for long-term disability benefits under his plan insured by Prudential. Prudential denied the claim.

Prudential took the position that the man was ineligible for benefits because his employment had ended, but his employment had ended because of the very disability for which he was seeking benefits, according to the lawsuit.

Chief District Judge Eric F. Melgren said Prudential's policy interpretation “borders on frivolous,” because it would “completely deny any benefits” to employees who resign, are fired, or transition to part-time work due to their disabilities.

The court ruled in favor of the employees and ordered Prudential to pay the benefits owed. The ruling exposes one of Prudential's claim denial tactics.

Prudential Long-Term Disability Complaints

Prudential is not accredited by the Better Business Bureau and has accumulated hundreds of consumer complaints on their BBB profile.

Policyholders who paid premiums for years describe a claims process designed to exhaust rather than resolve.

Common Prudential complaints include:

- Sudden Benefit Terminations: Claimants report receiving benefits for months or years before Prudential abruptly cuts off payments, often without adequate explanation and without any meaningful change in medical condition.

- Paperwork Delays and "Lost" Documents: A recurring complaint involves Prudential claiming forms, medical records, or physician statements were never received, triggering drawn-out investigations and payment freezes that leave claimants without income.

- Insufficient Objective Evidence: Claim denials cite a lack of clinical documentation, even when treating physicians have consistently supported the claim and submitted detailed records.

- Overriding Treating Physicians: Company-hired doctors may discount the documented limitations of claimants with complex conditions, including fibromyalgia, autoimmune disorders, and chronic pain, in favor of conclusions that serve Prudential's bottom line.

- Unexplained Delays: Claimants describe waiting months for decisions, receiving no meaningful updates, and being unable to reach anyone with authority to move their claim forward.

One policyholder described having her Prudential LTD claim closed after 14 months despite multiple disabilities, including autoimmune disorders, psoriatic arthritis, fibromyalgia, migraines, and memory issues. Prudential claimed they had never received paperwork, even though her doctor's office confirmed the records had been sent.

If any of these experiences sound familiar, you may have options. A Prudential disability lawyer can review your denial, identify where the process broke down, and help you decide whether an appeal or lawsuit is the right next step.

How Our Prudential Disability Attorneys Can Help

Prudential disability lawyers level the playing field against large insurance companies by handling claim denials, appeals, and ERISA lawsuits.

They ensure strict deadlines are met, gather comprehensive medical evidence, and fight common delay tactics to help you secure the LTD benefits you deserve.

A Prudential long-term disability appeal attorney on our team can:

- Decode the Denial: Prudential's denial letters are often written in technical policy language designed to hide the real reason your claim was rejected. We cut through the language and identify exactly what Prudential is relying on and where their reasoning is weakest.

- Build the Medical Record Prudential Can't Ignore: One of Prudential's most common denial tactics is arguing that the medical evidence doesn't meet the definition of disability. We work with your treating physicians to make sure your records document not just your diagnosis, but the specific functional limitations that prevent you from working.

- File Your Appeal or Take Prudential to Court: ERISA requires claimants to exhaust Prudential's internal appeals process before filing a lawsuit. Our attorneys prepare and submit appeals built for litigation, and take the next step to federal court when Prudential refuses to pay what they owe.

- Handle Every Interaction with Prudential: We manage all communications with Prudential on your behalf, ensuring nothing is said or submitted that could be used against your claim.

- Meet Every Deadline: Prudential's policy language includes lawsuit deadlines that federal courts have deemed confusing. Missing even one deadline can permanently eliminate your right to benefits. We track every date and make sure nothing slips.

Prudential has the resources to fight every claim for as long as it takes. You should not have to face that alone.

Our team builds strong cases and advocates for the LTD benefits you're entitled to. There are no upfront costs to have us manage the process on your behalf.

How Much Do Prudential Long-Term Disability Appeal Attorneys Charge?

At Sokolove Law, our Prudential long-term disability appeal attorneys handle cases on a contingency-fee basis. That means there are no upfront costs or hourly fees to have your claim reviewed or your appeal prepared.

We only get paid if we successfully recover disability benefits for you through a settlement, successful appeal, or lawsuit because we understand the financial strain a disability denial can create.

Our team can explain your legal options, answer your questions, and determine whether we may be able to help — all at no upfront cost to you.

Find a Prudential Disability Lawyer Near You

As a national law firm, we have the resources and experience to help individuals facing an unfair Prudential denial, regardless of where they’re located in the United States.

Our Prudential disability lawyers can help families in all 50 states:

- Alabama

- Alaska

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming

Insurance companies have entire teams working around the clock to protect their profits. You deserve someone fighting just as hard for you and the benefits you’ve paid for. Contact us now to find a Prudential lawyer near you.

Get Help with Your Prudential Long-Term Disability Appeal

With Sokolove Law on your side, you do not have to take on Prudential alone. If your long-term disability claim was denied, our team can help manage the appeals process, gather supporting evidence, and pursue the benefits you may be entitled to.

Why work with Prudential LTD appeal attorneys at Sokolove Law?

- Over 45 years of experience helping clients navigate complex disability claims and appeals

- More than $148 Million total recovered on behalf of clients nationwide

- Experience handling ERISA disability appeals and lawsuits against major insurance companies

Call (800) 995-1212 now or fill out our contact form for a free, no-obligation case review. We're available 24/7.

Prudential Disability Insurance Attorney FAQs

Can I appeal a Prudential disability denial?

Yes. If Prudential wrongfully denies your long-term disability claim, you generally have the right to appeal. Many families work with a Prudential long-term disability appeal attorney to help strengthen their case, gather supporting evidence, and ensure important deadlines are not missed.

Because Prudential disability appeals are subject to strict time limits, it's important to act quickly. Get started now with a free case review.

How long does Prudential long-term disability last?

The length of Prudential long-term disability benefits depends on the terms of your specific policy and the nature of your disabling condition.

Many Prudential LTD policies pay benefits:

- For a defined period, such as 2, 5, or 10 years

- Until you reach Social Security retirement age

- For as long as you continue to meet the policy's definition of disability

Reviewing your plan documents is the best way to understand how long benefits may be available under your specific coverage.

Why did Prudential deny my disability claim?

Prudential disability denials rarely come with a straightforward explanation. The stated reason in a denial letter is often technical, vague, or just one piece of a larger pattern.

Common reasons Prudential may have denied your claim include:

- Your medical records don't meet the definition of "objective" evidence of disability

- A company-hired physician reviewed your file and reached a different conclusion than your treating doctor, without ever examining you

- Prudential determined that your condition falls under a pre-existing condition exclusion

- Your claim was denied based on surveillance footage or social media activity Prudential argues contradicts your reported limitations

- There were gaps in your treatment history that Prudential characterized as non-compliance

- Your condition is subject to a limited benefit period, such as the 24-month cap many policies apply to mental health and self-reported symptom conditions

- Prudential determined that under the stricter "any occupation" standard that kicks in after 24 months, you're capable of performing some type of work

Whatever reason Prudential gave for denying your claim, that reason can be challenged. Our team can review your denial letter, identify weaknesses in Prudential's position, and fight for the benefits you deserve if the denial was unfair.

Can I sue Prudential for denying my disability claim?

Potentially, yes. If Prudential denied your disability claim and you’ve already gone through the appeals process, you may be able to file a Prudential disability denial lawsuit.

In one case, Prudential was sued by a trauma surgeon who suffered serious injuries in a car accident. The insurer determined that she could work in a different job role and cut off her long-term disability benefits, but later agreed to a settlement to end the case.

What qualifies as a disability under Prudential's policy?

Prudential long-term disability insurance eligibility typically depends on whether your health condition prevents you from performing the duties required and whether your medical records document that limitation sufficiently.

Health conditions that often qualify as a disability include:

- Musculoskeletal conditions: Back injuries, spinal disorders, degenerative disc disease, arthritis, and joint conditions that limit mobility or the ability to sit, stand, or perform physical tasks

- Cancer: Many diagnoses qualify, particularly where treatment causes functional limitations that prevent sustained work

- Neurological conditions: Multiple sclerosis, Parkinson's disease, traumatic brain injury, and conditions affecting memory, concentration, or motor function

- Autoimmune and chronic conditions: Lupus, rheumatoid arthritis, psoriatic arthritis, and similar conditions causing chronic functional limitations

- Cardiovascular conditions: Heart disease and conditions requiring significant restrictions on physical exertion

- Mental health conditions: Depression, anxiety, post-traumatic stress disorder (PTSD), and bipolar disorder may qualify

- Chronic pain and fatigue: Fibromyalgia and chronic fatigue syndrome are among the most frequently disputed conditions in Prudential claims, often denied on the grounds that symptoms are self-reported rather than objectively confirmed

Having a qualifying diagnosis is only the first step. Prudential requires clinical evidence showing how your condition limits your ability to work — not just that it exists.

How do I find a Prudential disability denial lawyer near me?

If Prudential has denied your long-term disability claim, finding an attorney with specific experience handling Prudential denials can improve your chances of a successful outcome.

At Sokolove Law, our Prudential disability lawyers represent clients in all 50 states and have secured over $148 Million total for those facing wrongful denials.

How much does a Prudential appeal attorney cost?

At Sokolove Law, there are no upfront costs to work with our Prudential disability lawyers. We handle cases on a contingency fee basis, which means you pay nothing unless we recover benefits on your behalf.

This matters for disability claimants in particular. If Prudential has cut off your income, the last thing you should have to worry about is whether you can afford legal help. Our fee structure is designed so that cost is never a barrier to fighting back against an unfair denial.