What to Know About Guardian Disability Benefit Denials

Guardian long-term disability denials are often due to in-house medical reviews, strict interpretations of policy language, or allegations that a claimant no longer meets the policy's definition of disability. Even policyholders who have paid premiums for years may find their benefits denied or terminated.

What's important to know is that a Guardian long-term disability (LTD) denial doesn't always indicate the legitimacy of your case, and you do have the right to appeal.

Find out more about Guardian disability denials:

- Denial on first submission is often the norm, not the exception, with providers like Guardian. Across the insurance industry, roughly 6 in 10 disability claims are denied on initial review, but a first denial is rarely the final word.

- If you're facing a Guardian long-term disability insurance denial, you can file an appeal to challenge the insurer's decision as well as a lawsuit in some cases. Guardian disability denial lawyers can help you understand your options, strengthen your appeal, and find evidence to prove you qualify.

- Over the years, Guardian has been accused of relying on paper-only medical reviews that contradict treating physicians' opinions, terminating benefits when policies switch from "own occupation" to "any occupation," and using surveillance to build cases against legitimate claimants.

- Guardian Life Insurance Company of America provides coverage to millions of Americans across a range of insurance and financial products, making it one of the country's largest mutual insurance companies.

- In 2001, Guardian merged with Berkshire Life Insurance Company of America, expanding their individual disability insurance portfolio. Berkshire Life was known for issuing high-value policies targeting high-income professionals like doctors, lawyers, dentists, and executives.

- Insurance companies have a legal duty to act in good faith and fair dealing with their policyholders. If Guardian has failed to uphold that obligation, they may be acting in bad faith, and that has consequences.

- Guardian has accumulated more than $3.3 Million in penalties across 13 recorded violations since 2000, including insurance violations and discriminatory practices, according to a nonprofit watchdog.

Guardian Life Insurance Company built their reputation on a simple promise: As a policyholder-owned mutual company, they answer to their members and not Wall Street investors. But for the thousands of policyholders who have had their long-term disability claims denied or terminated, that promise can feel hollow.

A Guardian disability denial can put your finances in jeopardy, especially when you're not able to work — but a denial is not the final word. Our Guardian long-term disability lawyers can help families in all 50 states fight back.

5 Reasons for Guardian Disability Denials

Guardian LTD denials may result from a lack of objective medical evidence or pre-existing condition exclusions. Benefits may also be approved initially and then terminated when the policy transitions from "own occupation" to "any occupation."

While Guardian disability denials can be issued for a range of reasons, many have to do with the company's profits — not your ability to work.

Guardian claim denial tactics may include:

- Insufficient Medical Evidence: Claiming your records don't show how your condition prevents you from working or that they lack objective evidence like test results to support your reported limitations

- Change in Definition of Disability: Scrutinizing claims and terminating benefits when the policy's definition of disability changes from your inability to perform your "own occupation" to your inability to perform "any occupation" — a shift that typically occurs after 24 months of benefit payments

- Pre-Existing Condition Exclusions: Arguing that your disabling condition is related to a health issue that existed before your coverage began, even when the connection is questionable or unsupported by your medical history

- Policy Limitations: Denying or terminating benefits based on policy-specific caps, most commonly 24-month limits on claims related to mental health conditions or musculoskeletal disorders like back pain

- Administrative Issues: Arguing that you failed to follow a prescribed treatment plan, missed deadlines, or submitted incomplete documentation, voiding your claim regardless of the underlying merits

Guardian may use a combination of these tactics to make the claims process confusing and discouraging, hoping that you'll give up before securing the LTD benefits you've paid for.

However, the Guardian disability lawyers at Sokolove Law know the tactics insurance companies use to deny valid claims — and how to fight back in order to get policyholders the results they deserve.

"Many clients come to me after their disability claim has been denied, and they’re often at their breaking point. They’re dealing with serious health complications, struggling to pay their bills, and facing a system that can feel stacked against them. That’s where a bad faith insurance attorney can make a real difference."

– Ricky LeBlanc, Managing Attorney of Sokolove Law

What to Do After a Guardian Long-Term Disability Denial

If you're facing a Guardian long-term disability denial, you typically must file a formal ERISA appeal within 180 days. Common reasons for Guardian denials include lack of objective medical evidence, pre-existing condition exclusions, and disputes over whether you can work in “any occupation.”

The steps you take in the days and weeks after a denial can significantly affect the outcome of your appeal or lawsuit. With 45+ years of experience helping families secure LTD benefits, we have what it takes to pursue the benefits you deserve.

If you've received a Guardian LTD denial, we may be able to help you:

- Understand Your Rights Under ERISA: Most employer-sponsored disability plans are governed by a federal law known as ERISA, which gives you the right to appeal Guardian's decision and holds the insurer to specific procedural requirements.

- Decipher Your Denial Letter: Guardian is required to tell you exactly why your claim was denied and when your appeal deadline expires. The reasons stated will shape the evidence needed to build a successful appeal.

- Obtain Your Claim File: You have a legal right to obtain every document Guardian relied on in making their decision: medical reviews, internal notes, and more. What's in that file often reveals the weaknesses in Guardian's position.

- Strengthen the Medical Record: A strong appeal goes beyond what you already submitted. Updated physician statements, functional capacity evaluations, and independent medical opinions can fill the gaps Guardian used to justify their denial.

- File Before the Deadline: Under ERISA, you typically have 180 days from the denial to file an appeal. Miss that window, and you may lose your right to pursue benefits entirely.

- Get Legal Help: An experienced Guardian disability attorney can manage the entire process, from gathering evidence to filing a potential lawsuit.

With the long-term disability denial attorneys at Sokolove Law handling every step of the process for you, you can focus on your health during this difficult time.

"Thanks to Sokolove Law, we won the battle against the insurance company. Now, I have the support and financial security I need to focus on my health and well-being. I'm grateful for their help and would recommend Sokolove Law to anyone facing a similar struggle."

– Engineer in D.C. with a Denied Disability Claim

What to Expect with Your Guardian Disability Appeal

A Guardian disability appeal is typically a paper-based process, not a courtroom hearing. Instead of appearing before a judge, you submit additional documentation for Guardian’s reviewers to reconsider your claim.

Under ERISA, you have to exhaust this internal appeal before you can file a lawsuit, meaning you must submit new medical records, functional capacity tests, and physician statements rebutting the specific reasons for denial.

The Guardian disability appeal process typically involves:

- Understanding Your Deadline: You typically have 180 days from the date of Guardian's denial letter to file your appeal. That clock starts immediately, and Guardian has been known to delay issuing denials or request rounds of additional documentation, which can eat into the time you have.

- Requesting Your Claim File: Before you can build a strong appeal, you need to know exactly what Guardian reviewed. What you find often reveals the specific gaps the appeal needs to fill.

- Gathering New Evidence: Your appeal needs to include updated medical records, functional capacity evaluations, detailed physician statements, and any expert reports that directly address Guardian's stated reasons for denial.

- Preparing Your Appeal: By submitting paperwork that's properly prepared, organized, and that rebuts Guardian's reasons for denial, you can improve your chances of a favorable outcome.

- Receiving a Decision: Guardian typically issues appeal decisions within 45 to 90 days. If the appeal is denied, you may have the right to file a Guardian disability lawsuit.

The complexity of this process is exactly why consulting a Guardian disability attorney before filing your appeal is strongly recommended. Our team can help families in all 50 states file appeals built to win and support a potential lawsuit.

Who Can File a Guardian Disability Lawsuit?

If you're a Guardian long-term disability policyholder whose benefits were wrongfully denied and have exhausted the appeals process, you may be eligible to file a Guardian disability lawsuit.

Federal courts have repeatedly found in favor of policyholders when Guardian failed to conduct a fair review, ignored treating physicians, or applied policy terms unreasonably.

You may have grounds to file a Guardian disability lawsuit if:

- Guardian denied your long-term disability claim, and you've exhausted the internal appeal process

- The denial contradicts the terms of your policy or isn't supported by the medical evidence in your file

- Guardian's reviewers dismissed your treating physician's opinion without adequate justification

- Your medical records document a condition that prevents you from working

Time is a factor. Statutes of limitations govern how long you have to file, and once that window closes, so does your right to pursue the benefits you're owed.

If you believe Guardian wrongfully denied your claim, don't wait to find out where you stand. Get a free case review now.

How to File a Guardian Long-Term Disability Appeal or Lawsuit

Under ERISA, you generally have 180 days from the date of your Guardian denial letter to file an appeal, which is mandatory before filing a lawsuit. The process typically involves requesting your claim file, gathering new evidence, and addressing the reasons for denial.

The Guardian's long-term disability appeal process is strict. Miss a deadline, submit weak evidence, or fail to address the right issues, and you're unlikely to secure the benefits you deserve.

At Sokolove Law, we walk clients through the entire process — from the initial appeal to a potential Guardian disability lawsuit.

Call (800) 995-1212 now to see if our Guardian disability attorneys may be able to fight for your LTD benefits. It costs nothing to speak with us.

1. Understand Your Deadline

From the date on Guardian's denial letter, you typically have 180 days to file a written appeal. That's a hard deadline under ERISA guidelines, and missing it can mean losing your right to pursue benefits.

What makes this trickier with Guardian is that the company has been known to draw out the denial process with repeated documentation requests, which can compress the time you have to prepare a thorough response.

Our team tracks every critical deadline from the start of your case through its resolution, helping protect your right to appeal or take legal action if necessary.

2. Read the Denial Letter and Pull the Claim File

Before you can build an appeal, you need to understand what you're appealing. Guardian's denial letter must state the specific reasons your claim was rejected.

Pair that with a request for your complete claim file. That file contains every medical review, internal note, and piece of evidence Guardian used to reach their decision.

Our Guardian disability lawyers can review:

- Every stated reason for denial

- How Guardian is interpreting your policy's definition of disability

- Evidence that was overlooked, mischaracterized, or never requested

- Where the gaps are and how to fill them

Once your lawyer has analyzed this information, they can craft a strategy to challenge the denial and pursue the benefits you deserve.

3. Gather New Evidence

Under ERISA, the evidence submitted during the administrative appeal is generally the only evidence that can be used if the case proceeds to federal court. There are no do-overs.

A complete Guardian appeal record should include:

- Updated medical records and treatment notes that reflect your current condition

- Detailed letters from treating physicians that speak specifically to your functional limitations and inability to work

- Functional Capacity Evaluations that document what you can and cannot do physically

- Vocational expert reports addressing your ability to perform your occupation or any occupation

- Personal statements from you, family members, or coworkers describing how your condition affects daily life

The appeal letter itself must directly address each reason Guardian cited for the denial — not in general terms, but with specific evidence that dismantles their position point by point.

4. Wait for Guardian's Decision

Once your appeal is submitted, Guardian assigns new reviewers, and decisions typically come within 45 to 90 days.

Our team manages all communications with Guardian during this period. Unreasonable delays in processing an appeal can themselves be evidence of bad faith — and we pay attention to how Guardian handles the clock.

5. File a Guardian Company Lawsuit

A denied appeal isn't necessarily the end of the road. Depending on your Guardian insurance policy and circumstances, a second appeal or a Guardian denial lawsuit may be possible.

At that stage, the administrative record you built becomes the foundation of the legal case, which is why the quality of that record matters as much as the outcome of the appeal itself.

Guardian has a legal team dedicated to defending its decisions. You should have one dedicated to challenging them. Guardian disability denial lawyers can fight on your behalf.

Since 1979, Sokolove Law has helped thousands of families nationwide secure the compensation they deserve.

Get a Free Case Review

Guardian Disability Settlements & Lawsuit News

Guardian disability settlements and verdicts vary based on the specific facts of each case. The strength of the medical evidence, your policy terms, and the nature of your disability can all play a role in the outcome.

Find out more about a few of the latest Guardian denial updates:

- A federal court ruled against Guardian after an internal memo surfaced describing high-cost disabled policyholders as "dogs" and "trainwrecks."

- Guardian paid $2 Million to state regulators after a multistate investigation found they failed to use a federal death database to identify deceased policyholders and pay life insurance benefits to their families.

- A Florida federal court found that Guardian paid a claimant disability benefits for 4 years, then handed him the medical evidence used to deny his claim on the same day as the insurance denial, leaving him no chance to respond.

- A federal appeals court ruled that Guardian collected premium payments for 26 months after their right to cancel a policy had vested and then denied the death claim after the policyholder died of cancer.

In one case, our team secured $45,000 for a purchasing manager at a chemical engineering company facing a Guardian disability denial.

Guardian denial lawsuits and court rulings provide insight into how the company handles claims and why certain denials are overturned. Compensation from a Guardian lawsuit can provide critical financial support while you’re unable to work.

Guardian Called Disabled Policyholders 'Dogs' and 'Trainwrecks'

Guardian canceled an entire class of small-group insurance policies across New York, New Jersey, South Carolina, and Colorado — policies identified as generating the highest claims.

Among those losing coverage was a New York man with muscular dystrophy who had lived on a ventilator for 18 years and required 24-hour nursing care costing approximately $1 Million per year. His father had purchased the policy in 1981.

During the lawsuit that followed, an internal Guardian memo described high-cost policies like his as "dogs" and "trainwrecks." A federal judge ruled Guardian had the right to end the plan, but the public backlash caused Guardian to continue covering patients in similar situations.

The controversy prompted the New York legislature to pass "Ian's Law," which now requires insurers to offer comparable replacement coverage before canceling any insurance plan.

$2 Million Guardian Settlement for Failing to Pay Life Insurance Benefits

A multistate investigation found Guardian used the Social Security Administration's Death Master File to stop annuity payments to deceased retirees but not to identify deceased life insurance policyholders and pay their families.

Guardian paid $2 Million to participating states and agreed to reform their practices. The settlement was part of a broader industry reckoning: Dozens of insurance companies entered similar agreements, returning nearly $10 Billion to beneficiaries.

Guardian Unjustly Denied LTD Benefits After 4 Years of Payments

A shipping supervisor reportedly received long-term disability benefits from Guardian for approximately 4 years after he had suffered a transient ischemic attack before the insurer cut them off in July 2020.

On appeal, Guardian's own peer physician reports concluded there was no evidence of physical impairment. However, Guardian shared those reports with the claimant on the same day as the final denial letter, making it impossible for him to review or respond to the evidence.

In 2024, a Florida federal court found Guardian had violated ERISA's full and fair review requirement, which mandates that claimants receive all evidence used against them in time to respond before a final decision is issued.

Guardian Collected Premiums but Denied Death Claim

A small business owner in Mississippi was diagnosed with cancer in 2019 and died in 2022. Her husband filed a Guardian life insurance claim but was told the policy had been canceled because her salon's workforce had dropped to one employee, according to the lawsuit.

Guardian was accused of accepting premium payments for 26 months after their cancellation right vested. Neither the husband nor the insurance agent who sold the policy had ever received a cancellation notice, the lawsuit stated.

In 2025, the 5th Circuit ruled in the husband's favor, finding Guardian had waived their right to cancel by accepting those premiums.

Guardian Denied a Long COVID Disability Claim by Misapplying a Pre-Existing Condition

An art director in California allegedly began developing severe neurological symptoms in 2021, including a hyperkinetic movement disorder, cognitive deficits, and panic attacks linked by medical records to COVID-19.

Guardian denied his long-term disability claim, arguing the condition stemmed from a pre-existing condition excluded under the policy.

A judge ruled in the claimant's favor, finding Guardian had misapplied the exclusion and that his condition did not qualify as a pre-existing condition barring coverage.

Guardian Ordered to Pay Leukemia Patient $461,000 in Attorney Fees

A business cofounder diagnosed with leukemia reportedly received Guardian LTD benefits for years before the insurer terminated them, claiming he could earn more than 80% of his pre-disability income.

The dispute centered on whether his business partnership earnings counted toward his "insured earnings," a calculation that directly determined both his benefit amount and Guardian's justification for cutting him off.

A federal judge found Guardian had either misread their own plan or that the plan required reformation. In a follow-up ruling, the court awarded the man $461,402 in attorney fees based on Guardian's overbroad plan interpretation.

Judge Orders Guardian to Expose Doctors' Financial Conflicts of Interest

When Guardian denied an LTD claim and the claimant sued, he sought to depose the senior case manager who issued the original rejection and the appeals manager who upheld it.

He also sought financial records revealing the relationships between Guardian and the independent medical reviewers they relied on to conclude he could still work. However, Guardian refused to provide these records.

A Kentucky judge ordered the depositions to proceed and Guardian to turn over the financial data, ruling that questioning specific decision-makers is appropriate when bias or conflict of interest is at issue.

Guardian Disability Insurance Reviews & Complaints

Guardian is a company that claims to answer to their own members rather than outside shareholders. In practice, however, Guardian policyholders have increasingly reported a claims experience that feels adversarial rather than supportive.

Documented through Better Business Bureau filings, consumer reviews, and court records, Guardian disability complaints reveal consistent patterns of delayed decisions, inadequate communication, and denial tactics.

Here are common Guardian long-term disability complaints:

- Benefits terminated after years of payments: Multiple claimants have reported receiving disability benefits from Guardian for a year or more — only to have their benefits abruptly terminated when their policy shifted from the "own occupation" to the "any occupation" definition of disability.

- Denial based on paper reviews from doctors who never examined them: Guardian routinely relies on in-house or contracted physicians who review records only on paper without ever meeting or examining the claimant.

- Increasingly aggressive claims scrutiny: Guardian, which issues many individual disability policies through its subsidiary Berkshire Life, has been accused of employing claims handling processes that lead to higher denial rates, delayed approvals, and intense scrutiny, particularly on group policies.

- Repeated documentation requests for records already submitted: Policyholders report receiving multiple rounds of requests for the same medical records and forms, which has been characterized as a stalling tactic.

- Poor communication and unresponsive case managers: Guardian complaints across multiple platforms cite unreturned calls, unexplained delays, and case managers who are difficult to reach. Claimants report being left without updates during critical periods in the claims or appeals process.

Guardian disability insurance complaints are all too common. The insurer has accumulated 155 complaints with the Better Business Bureau in the last 3 years alone, with service issues, the category covering claims handling, representing the largest single complaint type.

How Guardian Disability Attorneys Can Help

Guardian disability attorneys help policyholders with filing, appealing, or litigating unfair claim denials. They fight against aggressive insurer tactics by obtaining your entire claim file, gathering medical evidence, and meeting strict ERISA deadlines.

That's why working with a Guardian disability insurance lawyer from Sokolove Law can make a real difference. Having an experienced legal team in your corner may improve your chances of securing the benefits you're owed.

A Guardian long-term disability attorney on our team can:

- Analyze Your Guardian Life Disability Insurance Denial: Denial letters often use complex policy language and selective medical evidence to justify cutting off benefits. We help identify the real reasons behind the denial and what evidence may strengthen your case.

- Develop a Comprehensive Appeal: A successful Guardian appeal often requires more than standard medical records. We can gather supporting documentation, physician statements, specialist evaluations, and vocational evidence to demonstrate how your condition affects your ability to work.

- Handle the Appeals Process from Start to Finish: Most disability policies require a formal appeal before a lawsuit can be filed. Our Guardian long-term disability appeal lawyers can manage the process from beginning to end, including preparing evidence, tracking deadlines, and dealing directly with the insurance company.

- File a Guardian Lawsuit: If the insurer continues to deny your valid claim, we can file a Guardian disability insurance lawsuit on your behalf and fight for your benefits in court.

Insurance companies like Guardian have extensive legal and financial resources behind their decisions. You shouldn’t have to take on that process by yourself.

At Sokolove Law, we work to hold large insurers accountable and help level the playing field for disabled workers. With no upfront costs or hourly fees, you can focus on your health while we handle the legal battle.

Find a Guardian Disability Lawyer Near You

As a national law firm, we have the resources and experience to help individuals facing an unfair Guardian denial, regardless of where they’re located in the United States.

Our Guardian disability lawyers can help families in all 50 states:

- Alabama

- Alaska

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming

Insurance companies have entire teams working around the clock to protect their profits. You deserve someone fighting just as hard for you and the benefits you’ve paid for. Contact us now to find a Guardian lawyer near you.

Get Help with a Guardian Long-Term Disability Appeal

With Sokolove Law, you can feel confident knowing your Guardian long-term disability appeal is being handled by an experienced legal team. We can manage every stage of the appeals process on your behalf, so you can focus on your health and daily life.

Why choose the Guardian disability benefit attorneys at Sokolove Law?

- Over 45 years of experience

- More than $148 Million total secured for clients nationwide

- No upfront costs or hourly fees

Call (800) 995-1212 now or fill out our contact form to get started with your appeal. We're here for you 24/7.

The Guardian Disability Claim Denial FAQs

Can I appeal a Guardian long-term disability denial?

Yes. If your Guardian Life Insurance Company of America long-term disability claim was wrongfully denied, you may have the right to challenge the decision through the insurer’s appeals process or file a lawsuit if your appeal is denied again.

Many families choose to work with a disability attorney to help strengthen their appeal, comply with filing requirements, and submit the medical and vocational evidence needed to support their claim.

Because Guardian disability insurance appeals are governed by strict deadlines, acting quickly is important. Get a free case review now to learn about your legal options.

How does Guardian Life disability insurance work?

Guardian Life disability insurance is designed to provide partial income replacement if a medical condition prevents you from working.

In most cases, Guardian Life disability insurance works like this:

- You develop an injury, illness, or medical condition covered under your policy’s definition of disability

- You submit a claim supported by medical records, employment information, and other documentation

- After the policy’s waiting period, you may qualify for short-term disability benefits

- If the claim is approved, the policy typically pays a percentage of your income, often around 60%

- Benefits may continue for several years or until retirement age, depending on your coverage

Some Guardian policies provide benefits if you cannot perform your current occupation, while others require proof that you cannot work in any occupation at all.

Even after approving a claim, Guardian may continue reviewing your file for reasons to reduce or terminate benefits. Some claimants face unexpected denials after receiving payments for months or even years.

Does Guardian deny long-term disability claims?

Like many disability insurers, Guardian has faced allegations of unfairly denying legitimate long-term disability claims. Common issues include relying on in-house medical reviewers, terminating benefits during the transition to the stricter “any occupation” standard, and claiming there is insufficient objective evidence for conditions such as chronic pain or fatigue disorders.

Call (800) 995-1212 now if Guardian denied your claim. Our LTD lawyers may be able to help you challenge the decision through an appeal.

How long does Guardian insurance for disability last?

Guardian insurance for disability may last anywhere from a few years to retirement age, depending on the terms of your policy.

However, benefits can sometimes end earlier if Guardian claims you no longer meet the policy’s definition of disability, questions the medical evidence supporting your condition, or applies policy limitations.

If your benefits were terminated, a disability attorney may be able to help you appeal the decision and fight to restore your payments.

How much does Guardian short-term disability pay?

Guardian short-term disability pays a percentage of your regular income if you are temporarily unable to work because of a covered illness or injury.

Most Guardian short-term disability policies pay around 50% to 70% of your pre-disability earnings, though the exact amount depends on your employer’s plan and policy terms. Benefits are usually paid for a limited period, often a few weeks to several months.

Why did Guardian deny my long-term disability claim?

Guardian may deny a long-term disability claim for several reasons, including insufficient medical evidence, missed deadlines, or a determination that you do not meet the policy's definition of disability.

Common reasons why Guardian may deny a long-term disability claim include:

- Lack of supporting medical evidence: The insurer may argue that your records don’t fully explain how your condition prevents you from working.

- Failing to meet the policy’s definition of disability: Some plans become more restrictive over time, shifting from an “own occupation” standard to an “any occupation” standard.

- Pre-existing condition limitations: Guardian may deny benefits if the company believes your condition existed before your coverage took effect.

- Missed deadlines or paperwork issues: Strict filing requirements apply to many disability policies, and missing documentation can jeopardize a claim.

- File reviews by in-house doctors: Instead of conducting an in-person exam, Guardian may rely on internal medical reviewers who disagree with your treating physicians.

A denial does not automatically mean your claim lacks merit. With a strong appeal supported by medical and vocational evidence, it may be possible to challenge Guardian’s decision and pursue the benefits you deserve.

What are Guardian long-term disability qualifications?

In most cases, you must have an illness or injury that prevents you from working to meet Guardian long-term disability qualifications.

Conditions that may be covered by Guardian include:

- Cancer

- Carpal tunnel syndrome

- Cerebral palsy

- Chronic fatigue syndrome (CFS)

- Crohn’s disease

- Degenerative disc disease

- Diabetes

- Epilepsy

- Fibromyalgia

- Heart disease

- Lupus

- Mental health conditions, including anxiety and depression

- Multiple sclerosis (MS)

- Musculoskeletal disorders, like back or joint injuries

- Neurological conditions, including stroke or Parkinson’s disease

In some cases, patients diagnosed with one of these conditions may still be denied benefits by Guardian.

When that happens, a Guardian life disability insurance lawyer may be able to file an appeal or lawsuit on your behalf to seek the benefits you’re owed.

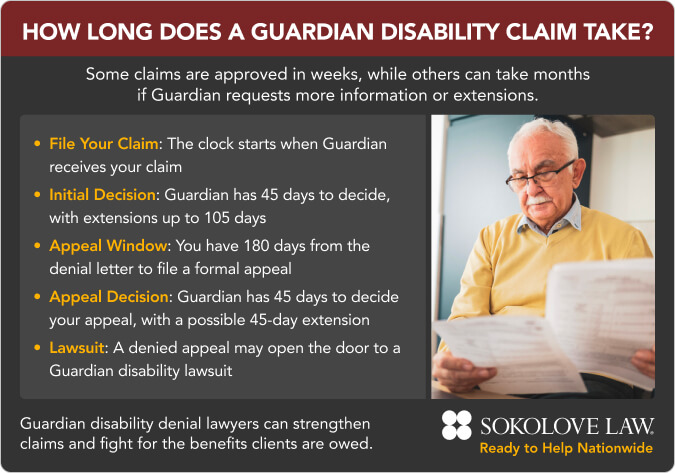

How long does it take Guardian to process a claim?

Under ERISA, Guardian is required to make an initial decision on a disability claim within 45 days of receiving it. They can extend that deadline by 30 days if they notify you in advance — and by another 30 days after that if more information is needed, bringing the maximum initial decision window to 105 days.

If Guardian denies your claim and you appeal, it has another 45 days to decide the appeal, with one possible 45-day extension for special circumstances.

How long does Guardian take to pay claims?

Once Guardian Life Insurance Company of America approves a long-term disability (LTD) claim, direct deposit payments are issued 2 business days after the processing date, according to the company’s documentation.

How do I fight a Guardian claim denial?

To fight a Guardian claim denial, you may be able to challenge the decision through the company’s formal appeals process. The first step is usually reviewing the denial letter carefully to understand why benefits were denied and what evidence the insurer claims is missing.

A strong appeal often includes updated medical records, detailed statements from your doctors, specialist opinions, and vocational evidence explaining how your condition limits your ability to work.

Because insurance companies often rely on complex policy language and internal medical reviews to justify denials, many people choose to work with a disability attorney to build a stronger case and protect their right to benefits.

Can I file a Guardian Company lawsuit over a denied claim?

Yes. If Guardian Company denied your disability claim and the appeal process does not resolve the issue, you may be able to file a lawsuit to pursue the benefits you believe you are owed.

Many employer-sponsored disability policies are governed by ERISA, a federal law that typically requires claimants to complete at least one formal appeal before filing a Guardian lawsuit.

A disability lawyer at Sokolove Law may be able to help evaluate your claim, manage the appeals process, and file a Guardian Company lawsuit if necessary.

How much do Guardian disability denial lawyers cost?

At Sokolove Law, our Guardian disability denial lawyers work on a contingency-fee basis, meaning you pay nothing upfront. Attorney fees are only collected if compensation or benefits are recovered for you. Contact us now to see if we can fight for you.